The UAE corporate tax regime, effective from 1 June 2023, has introduced a structured framework for taxing business profits. While the headline rate and thresholds receive most attention, one of the most important questions businesses and individuals must first answer is this:

Am I a taxable person under UAE corporate tax law?

Correctly identifying taxable person status determines whether you must register, file corporate tax returns, and pay tax. Misclassification can lead to non-compliance risks and penalties.

This guide explains who qualifies as a taxable person under UAE corporate tax law and who may fall outside its scope.

What Is a “Person” Under UAE Corporate Tax Law?

Under UAE corporate tax legislation, the term “Person” has a broad meaning. It generally includes both individuals and legal entities.

There are two primary types of persons:

Natural Person

A natural person refers to an individual human being. Under corporate tax rules, this includes individuals conducting business or commercial activities in the UAE.

Juridical Person

A juridical person refers to a legal entity created under law. This includes companies, corporations, partnerships with legal personality, and other entities established under UAE or foreign legislation.

Understanding this distinction is crucial because both natural and juridical persons may become taxable persons depending on their activities and status.

Who Is a Taxable Person?

A taxable person is any person required to:

- Register for corporate tax

- File corporate tax returns

- Pay corporate tax (if applicable)

Broadly, taxable persons fall into two categories:

- Resident Persons

- Non-Resident Persons

Each category has specific conditions that determine tax liability.

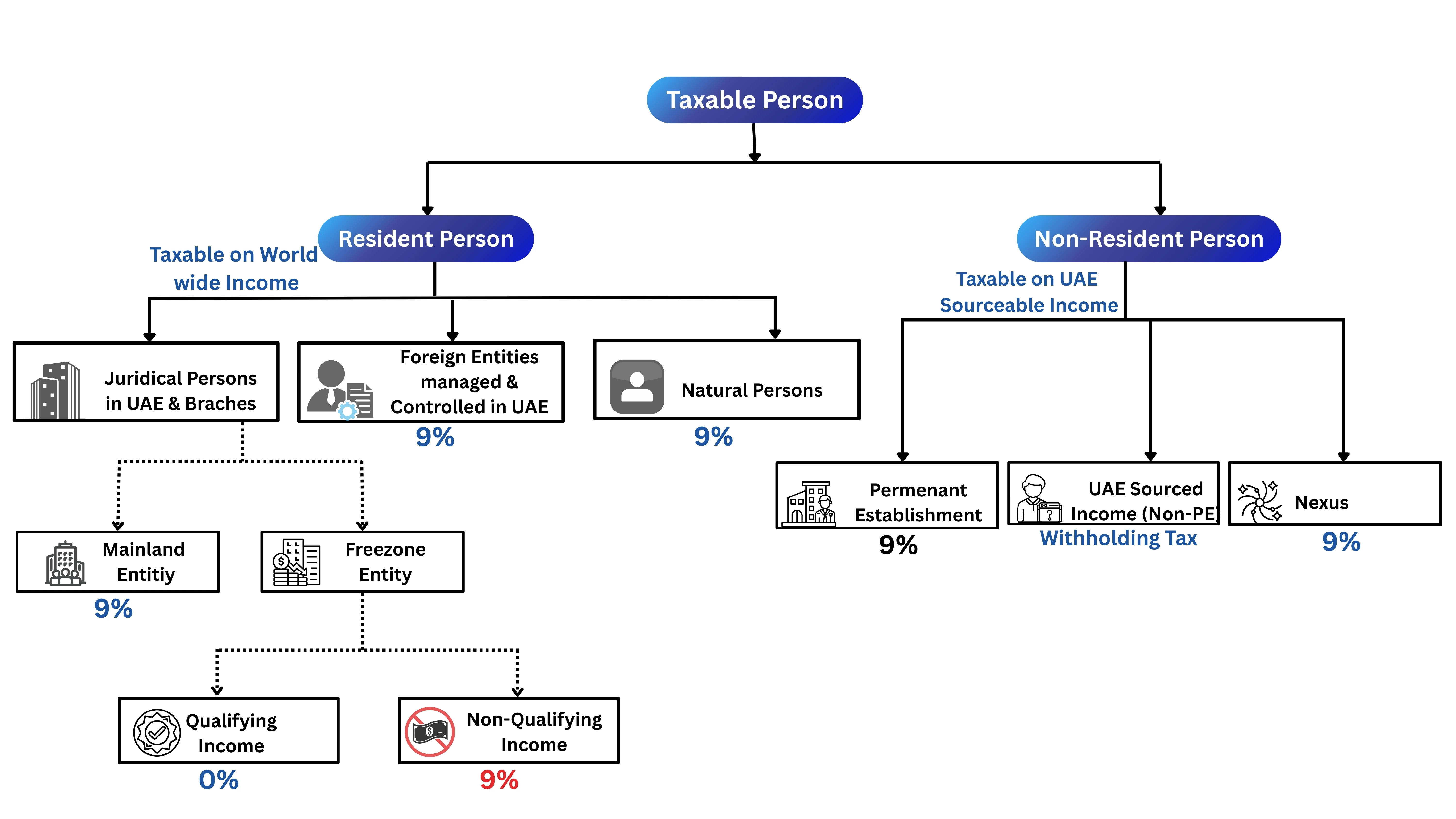

Resident Persons

A resident person is subject to corporate tax in the UAE based on residency criteria defined under the law.

Resident Juridical Persons

A juridical person is considered resident if:

- It is incorporated or established under UAE law (including mainland and free zone entities), or

- It is a foreign company that is effectively managed and controlled in the UAE

This means:

- Mainland companies are taxable persons.

- Free zone companies are also taxable persons (even if they may benefit from special rates).

- Foreign companies managed and controlled from the UAE may be treated as resident taxable persons.

Resident Natural Persons

Individuals conducting business or commercial activities in the UAE may also qualify as taxable persons.

However, corporate tax for natural persons generally applies only if:

- They are carrying on a business activity, and

- Their annual turnover exceeds AED 1 million

Passive personal income such as salary, personal investment income, or capital gains unrelated to a licensed business is generally not considered a taxable business activity.

This distinction is particularly important for sole proprietors and freelancers operating in the UAE.

Other Persons Identified by the Ministry of Finance

The UAE Cabinet or Ministry of Finance retains the authority to specify additional categories of resident taxable persons through formal decisions. Businesses should remain attentive to regulatory updates that may expand or clarify classifications.

Non-Resident Persons

Non-residents may also become taxable persons under certain conditions.

Non-Residents with a Permanent Establishment (PE) in the UAE

A non-resident entity becomes taxable if it has a Permanent Establishment in the UAE.

A Permanent Establishment may arise when a foreign business has:

- A fixed place of business in the UAE, or

- A dependent agent habitually concluding contracts in the UAE

In such cases, only income attributable to the UAE Permanent Establishment is subject to corporate tax.

Non-Residents Earning UAE-Sourced Income

A foreign entity deriving income from UAE sources may be subject to corporate tax depending on the nature of the income and applicable provisions.

Examples could include contractual income earned through activities connected to the UAE market.

Non-Residents with Nexus

A non-resident person may also be considered taxable if it has a sufficient economic nexus with the UAE.

This commonly applies to:

- Non-residents earning income from UAE immovable property

- Foreign entities generating income linked to assets located in the UAE

Special Considerations

Certain categories require additional clarification.

Free Zone Persons

Free zone companies are considered taxable persons under corporate tax law. However, they may qualify for a 0% corporate tax rate if they meet the conditions for being a Qualifying Free Zone Person.

Failure to meet the qualifying criteria may result in taxation at the standard 9% rate.

Branches of Taxable Persons

A branch of a UAE or foreign entity is not treated as a separate taxable person. Instead, it is considered part of the same taxable person as the head office.

For example:

- A UAE company’s branch is not separately taxable.

- A foreign company’s UAE branch may create a Permanent Establishment and become taxable accordingly.

Who Is Not a Taxable Person?

Certain entities are excluded or exempt under corporate tax law.

These may include:

- Government entities and government-controlled authorities

- Certain public institutions

- Approved non-profit entities

- Other exempt persons as defined in Cabinet decisions

Exemption does not necessarily eliminate registration or reporting requirements in all cases; specific conditions may apply.

Quick Reference Table

| Category | Taxable? | Notes |

|---|---|---|

| UAE incorporated company | Yes | Resident juridical person |

| Foreign company with PE in UAE | Yes | Non-resident taxable person |

| UAE individual running business | Yes | If turnover exceeds AED 1M |

| Passive income of individual | Generally No | Not considered business activity |

| Free zone entity | Yes | May qualify for 0% if eligible |

Why Correct Classification Matters

Identifying whether you are a taxable person is the first compliance step under UAE corporate tax.

Incorrect classification can lead to:

- Failure to register

- Late filing penalties

- Underreporting risk

- Increased audit exposure

Businesses should review their structure, activities, and income sources carefully to determine their status.

Conclusion

The UAE corporate tax system applies to many types of businesses, but it clearly separates resident and non-resident persons, natural persons (individuals doing business), juridical persons (companies), and exempt entities. Because of these differences, it is very important to understand whether your business qualifies as a taxable person under the law. This helps you register on time, file your tax returns correctly, plan your taxes properly, and avoid penalties or compliance problems. As corporate tax rules in the UAE continue to develop, businesses should regularly review their status to make sure they still meet the legal requirements. Identifying your tax position correctly today can help prevent serious regulatory issues in the future.